When does gap insurance not pay for mechanical repairs or routine maintenance? It also doesn’t cover unpaid loan balances due to late payments. Gap insurance, or Guaranteed Asset Protection insurance, is an optional coverage. It helps cover the difference between the amount owed on a vehicle and its actual cash value in the event of a total loss. This can be crucial for drivers who finance or lease their vehicles, as new cars depreciate quickly.

While gap insurance provides significant benefits, it’s important to know its limitations. It won’t cover mechanical repairs, routine maintenance, or unpaid loan balances due to missed payments. Understanding what gap insurance does and doesn’t cover helps drivers make informed decisions about their coverage needs.

Gap Insurance Does Not Pay When

The car isn’t declared a total loss. Comprehensive and collision coverage lapse. Policy exclusions apply (e.g., intentional damage or neglect). Negative equity from a previous loan isn’t covered. Loan payments are missed or late. The policy has expired. Always check specific policy terms for detailed exclusions.

What Is Gap Insurance?

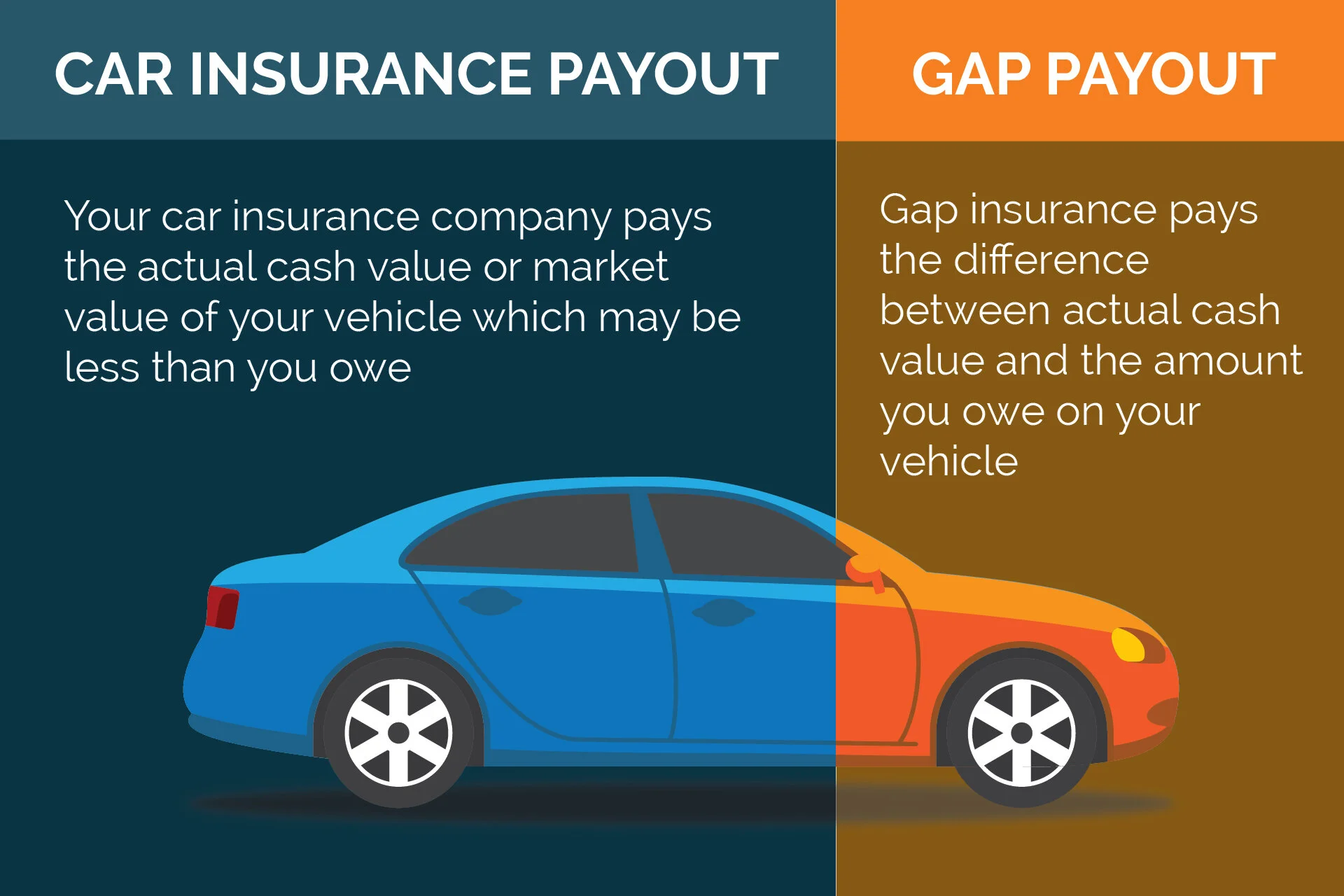

Gap insurance is extra car insurance. It helps when your car is totaled. It covers the gap between what you owe and the car’s value. When does gap insurance not pay stands for Guaranteed Asset Protection. It is useful if you have a loan or lease. When a car is totaled, regular insurance pays the market value. Sometimes, the market value is less than what you owe. This leaves a gap. Gap insurance covers this gap.

Common Misconceptions

Many think gap insurance covers everything. This is not true. It only covers the difference between the car’s value and the loan amount. Gap insurance is only for new cars or leased cars. It is not for old cars. Some think it covers the whole loan. It only covers the gap.

- It does not cover car repairs.

- It does not cover rental cars.

- It does not cover medical bills.

| Covered | Not Covered |

|---|---|

| Loan balance | Car repairs |

| Lease balance | Rental cars |

| Market value gap | Medical bills |

Non-covered Gap Car Insurance

When does gap insurance not pay offers essential protection for vehicle owners. But it doesn’t cover every car. Understanding non-covered vehicles can save you time and money. When does gap insurance not pay often exclude older models? Insurers deem them too risky. Cars more than 10 years old usually fall into this category. Their value depreciates significantly over time. Insurers find it hard to justify the risk.

| Vehicle Age | Coverage Status |

|---|---|

| 0-5 years | Covered |

| 5-10 years | Maybe Covered |

| 10+ years | Not Covered |

High-mileage Cars

High-mileage cars also fall under non-covered vehicles. Cars with more than 100,000 miles are risky. They have more wear and tear. This makes them less valuable and more prone to breakdowns. Understanding these exclusions can help you make informed decisions. Always check your policy details to know what’s covered.

- Vehicles with 50,000 miles: Usually covered

- Vehicles with 75,000 miles: Maybe covered

- Vehicles with 100,000+ miles: Not covered

Situations Involving Fraud

When does gap insurance not pay is a valuable safety net. It covers the difference between your car’s value and what you owe. But, there are scenarios where it won’t pay out. Fraudulent activities are top on that list. Let’s explore these situations.

Intentional Damage

Intentional damage to your vehicle is a serious offense. Gap insurance will not cover damages if they are deliberate. When does gap insurance not pay investigate accidents thoroughly. If they find out you caused damage on purpose, they won’t pay. Always drive responsibly to avoid this scenario.

False Claims

Submitting false claims is another fraudulent activity. If you lie about an accident, your gap insurance won’t pay. Insurers have ways to verify claims. If they find discrepancies, your claim gets denied. Always provide accurate information to your insurer. To summarize, engaging in fraudulent activities leads to denied claims. Honesty is crucial when dealing with insurance. Protect your interests by staying truthful.

| Fraudulent Activity | Outcome |

|---|---|

| Intentional Damage | Claim Denied |

| False Claims | Claim Denied |

Policy Limitations

Gap insurance helps cover the difference between your car’s value and your loan. Yet, it doesn’t always pay out. Understanding policy limitations can save you from unexpected costs. This section will explore key limitations.

Coverage Caps

Coverage caps limit the maximum amount your policy will pay. If your car loan is higher than this cap, you must pay the difference. Always check your policy’s cap before buying.

| Policy Type | Coverage Cap |

|---|---|

| Basic Gap Insurance | $10,000 |

| Premium Gap Insurance | $15,000 |

Exclusion Clauses

Exclusion clauses list situations where gap insurance won’t pay. These clauses vary by provider. Common exclusions include. Review these clauses carefully to avoid surprises. Understanding exclusions helps you know when you’re covered.

- Intentional damage

- Non-original parts

- Driving under influence

Late Premium Payments

Understanding gap insurance is essential for vehicle owners. One crucial aspect to consider is late premium payments. Missing payments can impact your coverage significantly.

Lapsed Policies

If you miss a payment, your policy may lapse. A lapsed policy means you lose coverage. Without coverage, gap insurance will not pay for claims. This can leave you financially vulnerable.

Grace Periods

When does gap insurance not pay companies often provide a grace period. This is a short period after the due date. During this time, you can make a late payment. The grace period helps prevent a policy lapse. Paying your premiums on time is crucial. It ensures your gap insurance coverage stays active. Always check with your insurer about their grace period policy. Late payments can lead to losing your gap insurance benefits. Stay proactive to keep your policy in force.

- Set reminders for premium payments

- Enroll in automatic payments

- Contact your insurer if you face payment issues

| Scenario | Outcome |

|---|---|

| Payment within Grace Period | Policy remains active |

| Payment within the Grace Period | Policy lapses |

Excluded Incidents

Gap insurance often covers the difference between your car’s value and the loan amount. But there are certain incidents where gap insurance won’t pay. These are called excluded incidents. Understanding these can help you avoid surprises.

Natural Disasters

When does gap insurance not pay for damages caused by natural disasters? This includes events like earthquakes, floods, and tornadoes. If your car is damaged in a flood, gap insurance won’t cover the gap. You need separate coverage for natural disasters. Your regular car insurance might help with these situations.

Acts Of War

Another excluded incident is acts of war. This means damages from war events are not covered. If your car gets damaged during a war, gap insurance won’t pay. Acts of war include things like bombings, invasions, and military actions. Make sure you know what is covered and what is not.

Unapproved Modifications

Unapproved Modifications can void your gap insurance coverage. This can be a costly mistake. Understanding what counts as an unapproved modification is crucial. Your insurance might refuse to pay if your car has these changes.

Aftermarket Parts

Installing aftermarket parts can affect your insurance. These parts aren’t approved by your car’s manufacturer. Common aftermarket parts include new rims, spoilers, or custom lights. Insurers often see these parts as risky. They can make repairs more expensive. This can lead to a denied gap insurance claim.

Unauthorized Repairs

Using unauthorized repair shops can void your coverage. Insurers prefer approved repair shops. These shops follow strict guidelines. Unauthorized repairs might not meet these standards. This can result in a denied gap insurance claim. When does gap insurance not pay to keep your valid, avoid these unapproved modifications. Stick to manufacturer-approved parts and repair shops. This ensures your coverage remains intact.

| Modification Type | Impact on Gap Insurance |

|---|---|

| Aftermarket Parts | Can lead to claim denial |

| Unauthorized Repairs | Can void coverage |

Frequently Asked Questions For When Does Gap Insurance Not Pay

What Is Gap Insurance?

Gap insurance covers the difference between your car’s value and the remaining loan balance.

Does Gap Insurance Cover Engine Failure?

No, When does gap insurance not pay doesn’t cover mechanical issues like engine failure? It only covers loan balance differences after a total loss.

Will Gap Insurance Pay For A Stolen Car?

Yes, gap insurance will pay if your car is stolen and not recovered. It covers the loan balance difference.

Does Gap Insurance Cover Late Payments?

No, gap insurance doesn’t cover missed or late payments. It only covers the difference between the car’s value and loan balance.

Does Gap Insurance Cover The Deductible?

No, When does gap insurance not pay usually doesn’t cover your insurance deductible. It only addresses the loan balance gap after a total loss.

Is Gap Insurance Valid For Leased Cars?

Yes, When does gap insurance not pay is often used for leased cars. It covers the difference between the lease payoff amount and the car’s value.

Conclusion

Understanding when the gap insurance does not pay is crucial. It helps avoid unpleasant surprises during claims. Always read your policy details carefully. Be aware of exclusions and conditions. This ensures you are adequately covered. Stay informed and make smart insurance choices. This knowledge protects your financial interests effectively.